{kind=link}

The European Central Bank (ECB) he has missed two great chances to ease its restrictive monetary policy in time and prevent stagnation in the eurozone. He thus becomes co-responsible for its stunted growth, and for the fact that the landing at digestible types is not as smooth as he preaches.

Its president, Christine Lagarde, confessed on Thursday that she was not “sure that we had anticipated it”: she was referring to the drop in inflation to 1.7% in September, below the 2% sought. Not anticipating it was due to the fact that he misread his own figures, prey to the prejudices of the “hawks”.

The first graph says a lot. The overwhelming basic component of general inflation was energy. The pyramidal loop of its gray line reveals a steep upward path and subsequent vertical fall. It did not last long: in January 2021 it exceeded zero after a long year below; rose in the fall due to Russian tensions and peaked at 44.3% in March 2022, after the invasion of Ukraine. It endured a plateau until October (in which the Europeans countered Russian blackmail on gas and oil) until collapsing in the first part of 2023. In September it capped, at least 4.6%: it was the opportunity to reformulate the monetary strategy. It was lost. At that time the ECB warned about underlying inflation, expectations, salaries… without focusing on what was essential: energy.

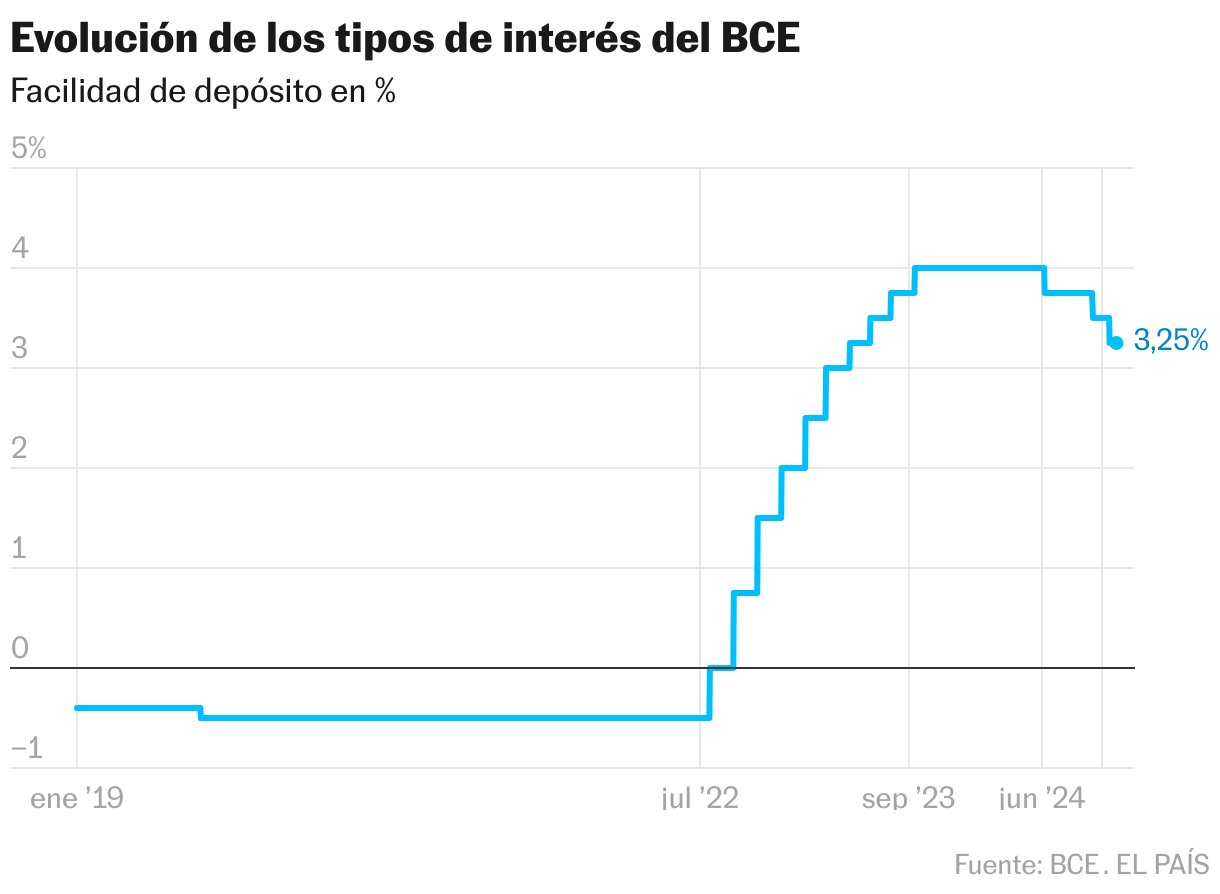

The general inflation (blue line) followed a similar, less steep pattern. Its worst peak came in October 2022: 10.6%. Since then it has fallen almost without rest until today. A key moment was its halving from January 2023 (8.6%) to September 2023 (4.3%): four points in eight months, at half a point per month. Just in that same September, doubly opportune to lower rates, Frankfurt decided to raise them for the last time.

Against the forceful (and discreet) warning of its internal doves, economic growth suffered. The Commission lowered it that month to an anemic 0.8% for 2023 and the ECB’s own economists to 0.7%, a fifth of 2022. And of the external ones. Like Joseph Stiglitz, who against the dominant criterion continued to maintain that inflation was temporary: long, but transitory, until the end of the energy supply and chip and freight crisis (Prices fall, despite central banksBusiness, 12/3/2023), or Manuel Alejandro (Chronology of the battle won by the team that defends temporary inflationCinco Días, 12/11/2023).

No case. Frankfurt would maintain high rates for another (almost) nine months, after having tightened them incessantly for fifteen (see the second graph). Until last June, when the first minimalist descent was scheduled. Even admitting that the increases would have been justified (although less so in their pace and intensity), those nine months of harshness made everything worse, a second missed opportunity. Germany repeats recession. The eurozone, asthenia. Fear of deflation spreads. And the ECB complains about “the recent downward surprises in activity indicators.” Surprises? Let them be surprised!